Home

Product

Pricing

Download App

Contact

Sign Up

Help Center

New

By

on

August 26, 2025

Blog |

Explore GST

|

Basics of GST

Sign Up for Free >

Featured Posts

Invoice Management System under GST: Features & Benefits

Cess tax: What it is and How it Affects Your Business

Auto-Population of E-Invoices into GSTR-1: Key Insights

GST rates and HSN code 204 for Meat Of Sheep, Goats.

Geyser, Water Heater HSN Code and GST Rate - 8516

Section 48 of CGST: Role of GST Practitioner

Goods Sent on Approval Basis Before Transition to GST

GST Expense Breakup in Tax Audit Report

You might also like

Digital Arrest Fraud in India: Modus Operandi, Recent Cases, and Prevention Tips

Learn how Digital Arrest Scams work in India, recent cases, and ways to protect yourself from this rising cyber fraud. Stay aware and stay safe.

GST on Bus Body Building & Tyre Retreading for SMBs

Learn GST rates, HSN codes, ITC rules, and compliance tips for bus body building and tyre retreading businesses in India.

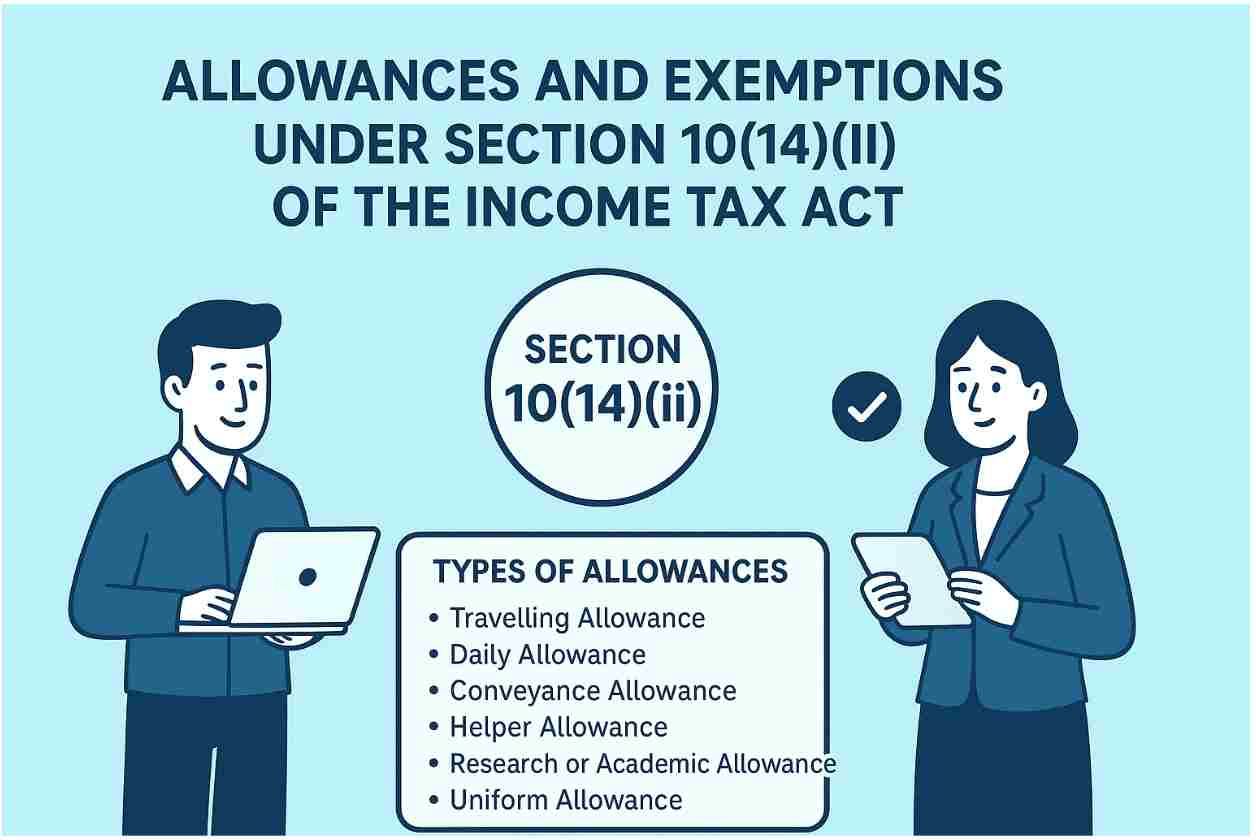

Allowances and Exemptions Under Section 10(14)(ii) of the Income Tax Act

Learn about allowances and exemptions under Section 10(14)(ii) of the Income Tax Act. Know the allowances, rules, limits, and how employees can claim tax benefits.

© 2026 Nextspeed Technologies. All rights reserved.

Privacy.

Join community.

.png)