Home

Product

Pricing

Download App

Contact

Sign Up

Help Center

New

By

Team Swipe

on

September 8, 2025

Blog |

Explore GST

|

More on GST

Sign Up for Free >

Featured Posts

Permanent Account Number (PAN): Full Form, Importance & Types

What is CRN Number: Meaning, Full form and How to find it

Filing Procedure Of Form FC-GPR

Intermediary Services Under GST: Taxation, Rules & Compliance Guide

Composition Levy Scheme in GST: Everything You Need to Know

Gift Vouchers: Why They Are Neither Goods Nor Services for GST

Appointment & Powers of Officers under GST

Tableware Kitchenware Plastics – GST Rates & 3924 HSN Code

You might also like

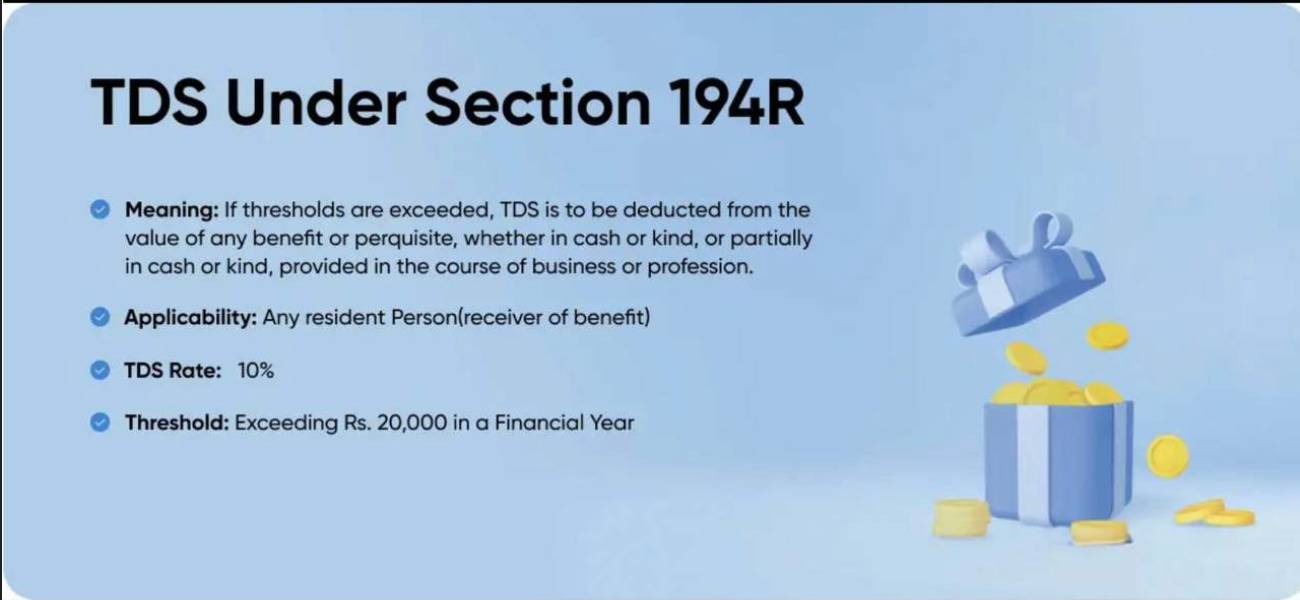

194R TDS: Rules, Rates, and Examples Explained

Learn Section 194R TDS rules, rates, applicability, and examples. Understand how TDS applies to business benefits and perquisites.

PM Internship Scheme: Opportunities For Students

Learn about the pm internship scheme and the opportunities it offers for students. Understand eligibility, stipend and career advantages

Amalgamation: Meaning, Objectives, Features, and Types

Discover the objectives of amalgamation, its meaning, features, types, and examples. Learn how businesses achieve growth and efficiency through amalgamation.

© 2026 Nextspeed Technologies. All rights reserved.

Privacy.

Join community.

.png)

-compressed.jpg)

-compressed.jpg)

.jpg)